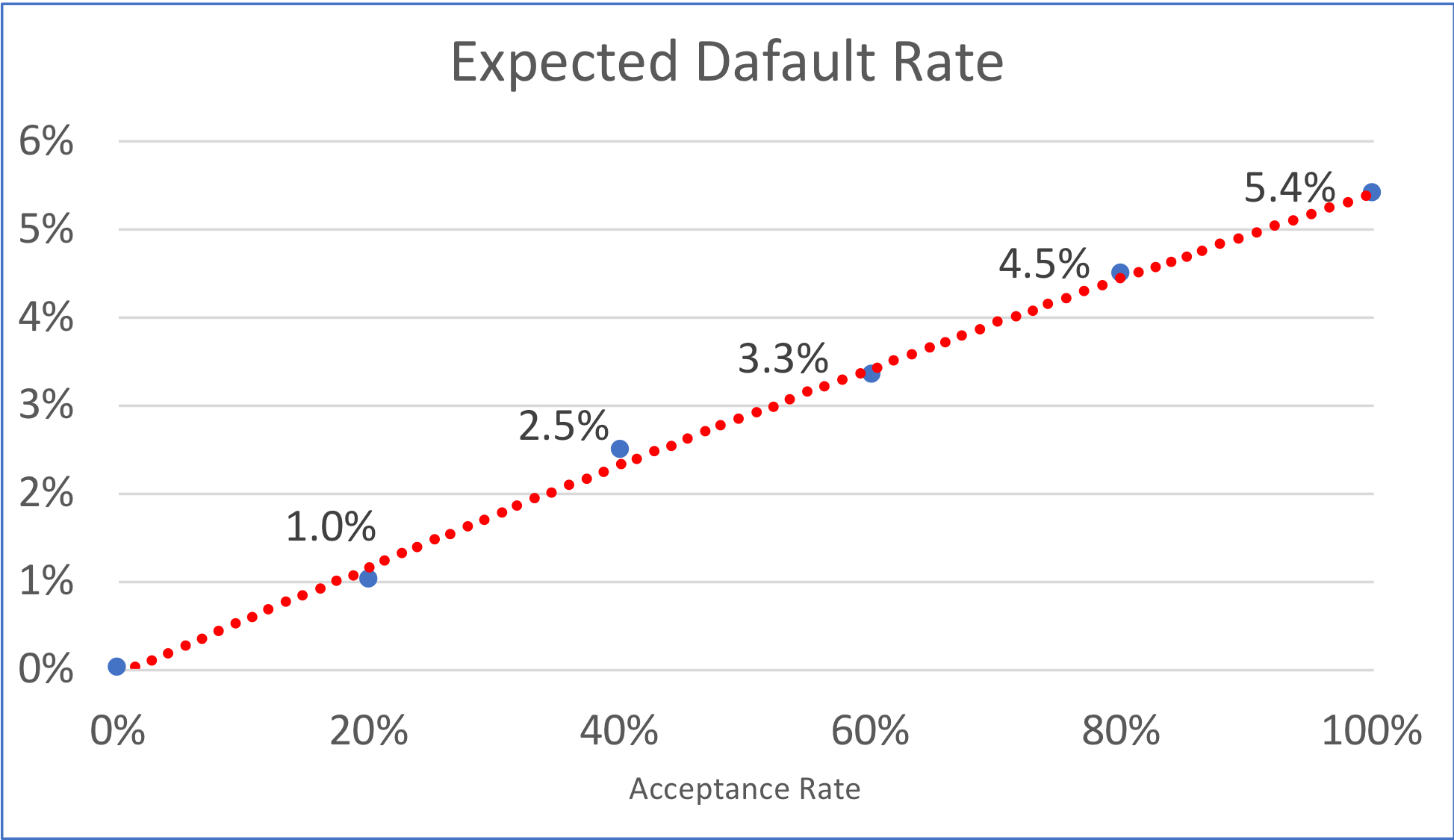

(English version below)

MicroBank, la entidad financiera española líder en microfinanzas en Europa, está evaluando constantemente sus procesos de cara al cliente, respecto a la usabilidad y la aceptación del usuario, una forma de actuar que supone una de sus prioridades. Cuando el banco desarrolla una innovación, se aplica el mismo nivel de escrutinio.

Entonces, cuando MicroBank decidió usar LenddoEFL para evaluar el perfil crediticio emprendedores para acceder a préstamos, el despliegue estaba condicionado a una experiencia positiva de sus clientes.

MicroBank empezó a medir la usabilidad del cuestionario de LenddoEFL, su impacto en el Net Promoter Score (NPS) con respecto al uso del microcrédito convenio entidades y cómo la gente se sentía al hacerlo.

Para nuestro agrado, encontramos que el cuestionario de LenddoEFL es fácil, comprensible y de duración apropiada. Acá se observan algunos puntos relevantes:

NPS: 84%, superando ampliamente nuestras expectativas

Satisfacción global: 9.16 de 10

Idoneidad: 82% encontró el cuestionario adecuado para evaluar a prestatarios del segmento micro. Esto es excelente comparado a las herramientas de la mayoría de los bancos, pero, obviamente, no dejamos de lado al 16% que no encontró el cuestionario adecuado. Nuestro equipo de producto trabaja 24 horas (literalmente, somos un equipo global) para mejorar constantemente nuestra evaluación de crédito – haciendo el contenido más fácil, más divertido, más rápido de completar, más predictivo y conveniente para todos los niveles de alfabetización y manejo de tecnología.

Duración: Más del 70% encontró que el cuestionario tiene la duración correcta. Esto es bueno, pero queremos mejorar.

Facilidad de uso: Más del 95% piensa que el cuestionario de LenddoEFL es fácil de completar.

MicroBank es un cliente exigente y este proceso nos ha ayudado a aprender y mejorar. Mientras que las noticias financieras están llenas de fintechs ayudando a bancos, este es un gran ejemplo de un banco mejorando a una fintech. Estamos muy contentos de que los resultados sean mejores de lo esperado, especialmente en un país como España, donde el acceso al crédito es generalmente bueno y la gente espera que el proceso se dé con la mínima fricción. Más aún, apreciamos que MicroBank nos haya desafiado para asegurar que nuestras herramientas superen las expectativas de sus clientes.

Esto nos hace mejores.

Para descargar el white paper completo por favor ingresa tu dirección de correo electrónico debajo.

LenddoEFL can predict risk, but do our clients like it? MicroBank evaluates the usability of LenddoEFL and the impact on NPS

MicroBank, the leading Spanish financial institution in microfinance in Europe, is constantly testing its client processes, regarding usability and user acceptance, ensuring these are always top priorities. When the bank launches an innovation, the same level of scrutiny applies.

So, when MicroBank decided to use LenddoEFL to assess the credit profile of entrepreneurs to access loans, the rollout was conditional on a positive customer experience.

MicroBank began to measure the usability of the LenddoEFL questionnaire, its impact on the Net Promoter Score (NPS) regarding the use of entities agreement microcredit, and how people felt about doing it.

MicroBank found the LenddoEFL questionnaire to be easy, understandable, and of appropriate duration. Here are some highlights:

NPS: 84%, far exceeding our expectations

Overall satisfaction: 9.16 out of 10

Adequacy: 82% found the appropriate questionnaire to evaluate micro-segment borrowers. This is excellent compared to the tools of most banks, but obviously we will not leave out the 16% who did not find the questionnaire suitable. Our product team works 24 hours (we are literally a global team) to constantly improve our credit assessment - making content easier, more fun, faster to complete, more predictive and more suitable for all levels of literacy and access to technology.

Duration: More than 70% found that the questionnaire was the right length. This is good, but we are working to reduce this.

Ease of use: More than 95% think the LenddoEFL questionnaire is easy to complete.

MicroBank is a demanding customer and this process has helped us learn and improve.

While the financial news is full of FinTechs helping banks, this is a great example of a bank improving a FinTech. We are very happy that the results are better than expected, especially in a country like Spain, where access to credit is generally good and people expect the process to take place with minimal friction. Furthermore, we appreciate that MicroBank has challenged us to ensure that our tools exceed their customers' expectations.

This makes us better.